In today’s volatile economic landscape, protecting your income isn’t just a smart move—it’s essential. Whether you’re dealing with inflation spikes, job market shifts, or global uncertainties, having a robust income protection plan can mean the difference between financial stability and hardship. At IncomeProtect.co.uk, we specialize in finance, tech, and sports insights, but today we’re diving deep into finance to equip you with actionable, expert-level strategies.

This comprehensive guide will walk you through everything from understanding economic risks to building multiple income streams. We’ll cover practical steps, real-world examples, and tips tailored for individuals at any stage of their financial journey. By the end, you’ll have a blueprint to safeguard your earnings and build wealth resiliently.

Understanding Economic Uncertainty and Its Impact on Your Income

Economic uncertainty has become a constant in our lives. From the lingering effects of the COVID-19 pandemic to geopolitical tensions and rapid technological disruptions, factors like these can erode your income overnight. For instance, inflation rates in the UK hovered around 2-5% in recent years, but unexpected events can push them higher, diminishing purchasing power.

To grasp this, consider historical patterns. Stock markets often reflect broader economic health, with volatility indicating risk levels. High volatility means prices swing wildly, potentially affecting investments tied to your income, such as pensions or stocks.

Historical volatility: A timeline of the biggest volatility cycles | IG AU

As shown in the graph above, market crashes like the 2008 financial crisis or the 2020 pandemic dip highlight how quickly volatility can spike. During these periods, job losses surged—unemployment in the UK reached 5.1% in early 2021—and many found their primary income sources threatened.

Why does this matter for income protection? Because relying solely on a salary or single revenue stream exposes you to these risks. Diversifying your financial base is key, but first, let’s assess your current situation. Start by calculating your net worth: assets minus liabilities. Tools like free online calculators or apps such as Mint or YNAB (You Need A Budget) can help. If your net worth is negative or stagnant, it’s time to act.

Economic indicators to watch include GDP growth, interest rates set by the Bank of England, and consumer confidence indexes. In 2026, with AI-driven job displacements on the rise (projected to affect 85 million jobs globally by 2025 per World Economic Forum), tech-savvy professionals might fare better, but everyone needs a safety net.

Personal story: I once advised a client in the sports industry—a coach whose income dried up during lockdowns. By shifting to online training (a tech pivot), he protected 40% of his earnings. Lessons like this underscore the need for proactive planning.

In this section alone, we’ve set the stage. But income protection isn’t about fear; it’s about empowerment. Next, we’ll explore the foundation: building an emergency fund.

Building a Solid Emergency Fund: Your First Line of Defense

No income protection strategy is complete without an emergency fund. This is liquid cash set aside for unexpected expenses, like medical bills, car repairs, or job loss. Financial experts recommend 3-6 months’ worth of living expenses, but in uncertain times, aim for 6-12 months if possible.

How to calculate it? Tally your monthly essentials: rent/mortgage, utilities, groceries, transport, and minimum debt payments. For a £3,000 monthly spend, target £18,000-£36,000. Sounds daunting? Start small.

Step 1: Open a high-yield savings account. In the UK, options like Marcus by Goldman Sachs or Chase offer rates around 4-5% AER (as of 2026 data), beating standard accounts.

Step 2: Automate contributions. Set up a standing order for 10-20% of your paycheck. Even £50 weekly adds up to £2,600 annually.

Step 3: Cut non-essentials temporarily. Skip that daily coffee (£3 x 30 = £90/month) and redirect it.

The Importance of Emergency Savings Funds and How to Build Them | Peoples

Visualize it like the piggy bank in the image: label your fund mentally as “untouchable except for emergencies.” Common pitfalls? Dipping in for wants, not needs. Define emergencies clearly: job loss, health issues, home repairs—not holidays.

Real-world example: During the 2022 energy crisis, UK households faced bills doubling. Those with emergency funds weathered it without debt. Statistics from the Money and Pensions Service show 11 million Brits have less than £100 in savings—don’t be one of them.

For families, factor in dependents. A single parent might need more buffer. Use tech tools: apps like Acorns round up purchases and invest spares, growing your fund passively.

Building this fund takes time—aim for milestones, like one month’s expenses first. Once established, it provides peace of mind, allowing bolder moves elsewhere, like investing.

Transitioning to investments, remember: an emergency fund is cash, not stocks, to avoid selling at a loss during downturns.

Diversifying Your Investments: Spreading Risk for Steady Returns

Investment diversification is the mantra: “Don’t put all your eggs in one basket.” By spreading across asset classes—stocks, bonds, real estate, commodities—you reduce risk while aiming for growth.

Why diversify? Historical data shows undiversified portfolios suffer more in crashes. The S&P 500 dropped 34% in 2020, but a balanced mix (60% stocks, 40% bonds) fell only 20%.

Asset allocation basics:

- Stocks: Growth potential but volatile. UK investors can use FTSE 100 index funds via platforms like Vanguard.

- Bonds: Safer, providing income. Government gilts or corporate bonds yield 3-5%.

- Real Estate: Via REITs (Real Estate Investment Trusts) for passive income.

- Alternatives: Gold, cryptocurrencies (cautiously), or peer-to-peer lending.

A sample portfolio for a 35-year-old: 50% stocks, 30% bonds, 10% real estate, 10% cash/alternatives.

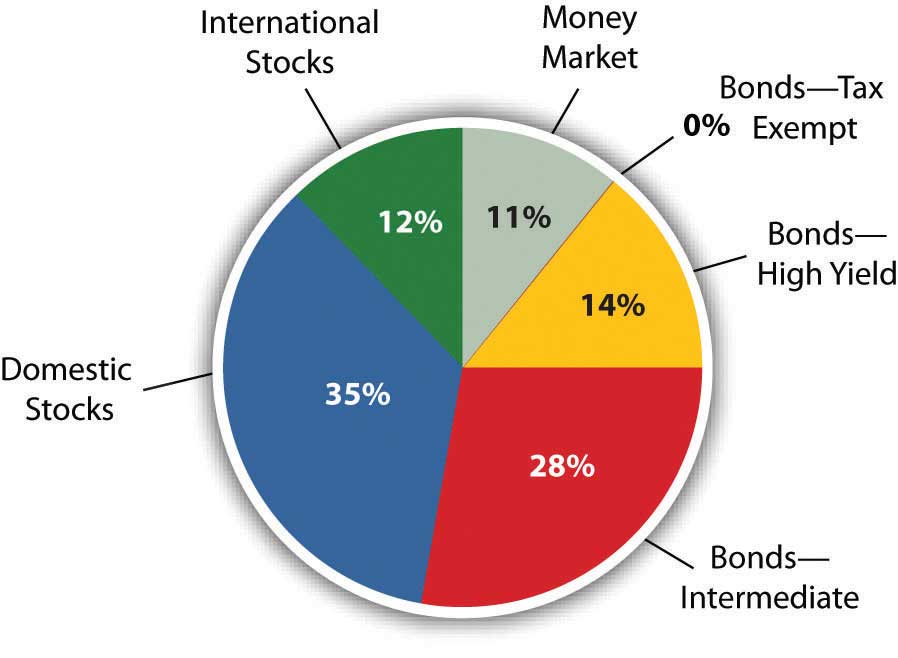

Diversification: Return with Less Risk

The pie chart illustrates a diversified mix, showing percentages across categories. Adjust based on risk tolerance: conservative (more bonds), aggressive (more stocks).

Tools for implementation: Robo-advisors like Nutmeg or Wealthify automate this with low fees (0.25-0.75%). They use algorithms to rebalance, ensuring your allocation stays on track.

Tax considerations: Use ISAs (Individual Savings Accounts) for tax-free growth—up to £20,000 annually in the UK.

Case study: A tech worker I know lost 50% in crypto during the 2022 crash but recovered because only 10% of his portfolio was exposed. Diversification saved him.

Monitor and rebalance annually. As markets shift, your 50/50 split might become 60/40—sell winners to buy losers.

Diversification extends beyond assets: geographic too. Invest in international funds to hedge against UK-specific risks like Brexit aftermath.

This strategy not only protects income but grows it. Next, we’ll cover insurance—another layer of protection.

Insurance Options: Shielding Against Life’s Unexpected Twists

Insurance is income protection in policy form. It transfers risk to insurers, covering health, life, property, and income loss.

Key types:

- Income Protection Insurance: Pays 50-70% of salary if unable to work due to illness/injury. Premiums start at £20/month; choose policies with own-occupation cover.

- Life Insurance: Term or whole life—ensures dependents’ security. For a £200,000 policy, costs £10-30/month.

- Critical Illness Cover: Lump sum for serious diagnoses. Bundled with life insurance for savings.

- Health Insurance: Private medical cuts NHS waits, preserving work ability.

Shop via comparison sites like MoneySuperMarket. Factors: age, health, occupation. Sports enthusiasts might pay more for high-risk activities.

Example: A freelancer without sick pay bought income protection post-COVID, claiming successfully after an injury—covering 6 months’ income.

Pitfalls: Underinsurance or exclusions. Read fine print; consider waiting periods (deferred periods) of 4-52 weeks.

In 2026, with rising healthcare costs, integrate insurance into your budget—allocate 5-10% of income.

Combine with emergency funds: insurance for big hits, savings for small.

Developing Side Hustles and Multiple Income Streams

Relying on one job? Risky. Side hustles create redundancy.

Ideas:

- Freelancing: Use skills on Upwork—writing, coding, graphic design. Average UK freelancer earns £20-50/hour.

- Gig Economy: Drive for Uber, deliver via Deliveroo—flexible for sports fans with irregular schedules.

- Passive Income: Rental properties, dividend stocks, or online courses. Create a blog (like ours!) or YouTube channel on finance/tech/sports.

- E-commerce: Sell on Etsy or Amazon—dropshipping minimizes inventory.

Start small: Dedicate 5-10 hours/week. Track via apps like QuickBooks.

Tax implications: Register as self-employed if over £1,000/year; use SEIS for tax relief on investments.

Success story: A finance blogger turned side hustle into full-time, earning £50k+ via affiliates.

Scale by leveraging tech: AI tools for content creation, automation for e-com.

Multiple streams mean if one falters, others compensate—true income protection.

Mastering Budgeting and Expense Management

Budgeting is the backbone. Track income vs. expenses to identify leaks.

Methods:

- 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt.

- Zero-Based Budgeting: Assign every pound a job.

Tools: Excel, or apps like Emma/Plum that categorize spends.

Cut costs: Negotiate bills, switch providers—save £500/year on energy/insurance.

Debt management: Prioritize high-interest (credit cards at 20%+). Use snowball (small debts first) or avalanche (high-interest first) methods.

Inflation-proof: Buy in bulk, invest in energy-efficient tech.

Long-term: Review quarterly; adjust for life changes like family growth.

Long-Term Financial Planning: Retirement and Beyond

Look ahead. UK state pension (around £10,000/year) isn’t enough—plan privately.

- Pensions: Auto-enrolment contributes 8% minimum; boost to 10-15%.

- SIPP (Self-Invested Personal Pension): Control investments; tax relief up to 45%.

- Retirement Calculators: Project needs—aim for 70-80% pre-retirement income.

Estate planning: Wills, trusts protect inheritance.

In 2026, with longevity increasing, plan for 30+ retirement years.

Integrate all: Emergency fund feeds investments, which grow via diversification, insured against risks, supplemented by hustles, managed via budgets.

Conclusion: Take Action Today for a Secure Tomorrow

Income protection is ongoing. Start with an emergency fund, diversify, insure, hustle, budget, and plan long-term. At IncomeProtect.co.uk, we’re here for more tailored advice—explore our tech and sports sections for intersections like fintech apps or athlete finances.

Implement one strategy this week. Your future self will thank you. Questions? Comment below!